How $300 Payday Loans Trap Canada’s Most Vulnerable Communities

When a single mother in Toronto borrows a $300 loan at RadCred to cover an unexpected childcare expense, paying back $390 two weeks later, she enters a financial arrangement that economists might explain through interest rates and market demand. But sociology reveals a different story: one of structural inequality, social exclusion, and the monetization of poverty itself.

Payday loans in Canada represent far more than emergency credit. They function as visible markers of deepening social stratification, where approximately 1.9 million Canadians annually access these high-cost loans despite interest rates that can exceed 400% APR. The industry generates over $2 billion in revenue, yet serves predominantly low-income neighborhoods, Indigenous communities, and newcomers to Canada who face systematic barriers to traditional banking. This isn’t coincidental. It’s structural.

The sociological lens transforms how we understand payday lending. Rather than viewing borrowers as making poor financial choices, sociology examines the institutions, power relations, and social forces that channel vulnerable populations toward predatory credit. Why do certain postal codes have five payday lenders within walking distance while others have none? How do gender, race, and immigration status intersect to determine who relies on these services? What does the normalization of 500% interest rates tell us about contemporary capitalism’s relationship with the working poor?

This analysis positions payday loans as a case study in financial marginalization, where emergency credit becomes a mechanism for extracting wealth from those who can least afford it. Drawing on Canadian regulatory data, borrower demographics, and theoretical frameworks from Pierre Bourdieu to Saskia Sassen, we’ll examine how payday lending both reflects and reproduces social inequality. The comparison with France, where payday loans remain largely prohibited, offers crucial insights into how different societies regulate the commodification of financial desperation.

The question isn’t simply why people borrow. It’s why our social systems produce conditions where such borrowing becomes necessary, normalized, and profitable.

The Payday Loan Industry in Canada: A Sociological Overview

Market Size and Geographic Distribution

Canada’s payday loan industry operates approximately 1,400 storefronts alongside a growing online presence, generating over $2 billion in annual lending volume. This geographic footprint reveals stark patterns of spatial inequality.

Payday loan outlets cluster disproportionately in neighborhoods characterized by lower median incomes, higher unemployment rates, and greater proportions of racialized residents. Research mapping Toronto’s payday lenders demonstrates that outlets concentrate in areas where household incomes fall below the city’s median, creating what geographers term “fringe financial services deserts” where traditional banks have withdrawn while alternative lenders proliferate.

Urban centers show the highest density, but the pattern varies by region. Ontario hosts approximately 40% of Canada’s payday loan outlets despite containing roughly 38% of the population, reflecting the province’s earlier deregulation of lending rates. Western provinces, particularly British Columbia and Alberta, show similar urban concentration patterns, with outlets clustering near transit hubs and social housing complexes.

Rural and remote communities face different dynamics. While fewer physical storefronts exist outside cities, residents often lack alternatives entirely. Indigenous reserves and northern communities, where traditional banking infrastructure remains sparse or absent, represent extreme cases of financial service gaps that online payday lenders increasingly target.

This geographic distribution is not coincidental. Payday lenders strategically locate where economic precarity meets limited banking access, positioning their services as necessary infrastructure in communities mainstream financial institutions have abandoned.

The Regulatory Patchwork Across Provinces

Canada’s fragmented regulatory approach to payday lending creates starkly different realities for borrowers depending on their province of residence. Unlike many countries with national consumer credit frameworks, Canada delegates payday loan regulation to provincial governments, resulting in a patchwork of rules that sociologically function as a form of “lottery of location” for vulnerable borrowers.

Provincial cost caps vary dramatically. Quebec banned payday loans entirely in 2017, while Manitoba caps costs at $17 per $100 borrowed. Ontario permits $15 per $100, Saskatchewan allows $17, and Alberta $15. British Columbia set its cap at $15 per $100, but some provinces like New Brunswick have no specific cost regulations for payday loans. For someone borrowing $300, the difference between Manitoba’s cap ($51 in fees) and an unregulated province (potentially $75 or more) represents a substantial burden on already strained budgets.

Beyond cost, provinces diverge on borrower protections. Some require extended repayment plans for repeat borrowers, while others lack such provisions. Maximum loan amounts, cooling-off periods between loans, and rollover restrictions differ substantially. Ontario prohibits more than one concurrent loan, but enforcement mechanisms vary across jurisdictions.

This regulatory inconsistency reflects competing provincial philosophies about poverty governance. Quebec’s outright ban represents a harm-reduction approach viewing payday loans as predatory, while provinces permitting the industry with cost caps operate under a consumer-choice framework that assumes borrowers make rational decisions within a constrained market. The sociological significance lies in how geography determines whether a $300 loan becomes a manageable emergency solution or the first step into a debt spiral, revealing how federalism can amplify rather than mitigate social inequality.

Social Stratification and Financial Marginalization

The Working Poor and Income Volatility

The working poor occupy a precarious position in Canada’s economic landscape, facing income volatility that makes budgeting nearly impossible and forces reliance on emergency credit. Unlike salaried middle-class workers who can anticipate their monthly earnings, low-wage workers frequently experience fluctuating hours, unpredictable schedules, and seasonal layoffs that create cycles of feast and famine. A retail worker might receive 35 hours one week and only 18 the next, with no advance notice. This unpredictability means that even employed Canadians struggle to align income with fixed expenses like rent, which don’t accommodate irregular paycheques.

The expansion of gig economy work has intensified these patterns. Delivery drivers, rideshare operators, and contract cleaners bear the risks that employers once absorbed, experiencing dramatic swings in weekly earnings based on demand, weather, or platform algorithm changes. When a utility bill arrives during a slow week, these workers face an immediate crisis that their bank balance cannot resolve. Traditional credit requires stable income verification, which gig workers often cannot provide despite working full-time hours.

This structural mismatch between income timing and expense timing pushes working-poor Canadians toward short-term payday credit as a stopgap solution. A $300 payday loan bridges the gap until the next pay deposit, allowing rent to be paid on time or keeping a car on the road for work commutes. From a sociological perspective, these borrowing patterns reflect not financial illiteracy but rational responses to income instability that the formal banking system fails to address. The working poor use payday loans because their employment conditions create temporal mismatches between earning and spending that no amount of budgeting can solve.

Banking Deserts and Financial Exclusion

The concept of banking deserts, geographic areas with limited or no physical access to traditional financial institutions, plays a crucial role in driving Canadians toward payday lenders. Research has documented that bank branch closures disproportionately affect low-income neighbourhoods, rural communities, and areas with higher concentrations of racialized populations. When the nearest bank branch requires a lengthy commute or multiple bus transfers, the convenience of neighbourhood payday loan outlets becomes a practical necessity rather than a choice.

This spatial dimension of financial exclusion extends beyond physical access. Even when bank branches exist nearby, many low-income Canadians face barriers to opening and maintaining accounts. Minimum balance requirements, monthly fees, and credit checks create gatekeeping mechanisms that exclude precisely those who most need basic banking services. A single overdraft fee can trigger account closures, leaving individuals with damaged banking records that prevent them from accessing mainstream financial institutions for years.

The rise of digital banking has not solved these access problems. Populations without reliable internet access, smartphones, or digital literacy skills remain excluded from online banking platforms that financial institutions increasingly favour. Older adults, those experiencing homelessness, and communities with poor internet infrastructure cannot easily participate in a banking system that assumes constant digital connectivity.

Payday lenders strategically locate their outlets in these banking deserts, offering immediate cash access without the bureaucratic requirements of traditional banks. They don’t require credit checks, minimum balances, or proof of stable address. For someone needing $300 to prevent utility disconnection, a payday lender two blocks away represents accessible financial services, however exploitative the terms. This geographic and institutional exclusion from mainstream banking transforms payday loans from predatory products into essential infrastructure for financial survival.

The $300 Threshold: Why Small Loans Matter

Emergency Expenses and Survival Debt

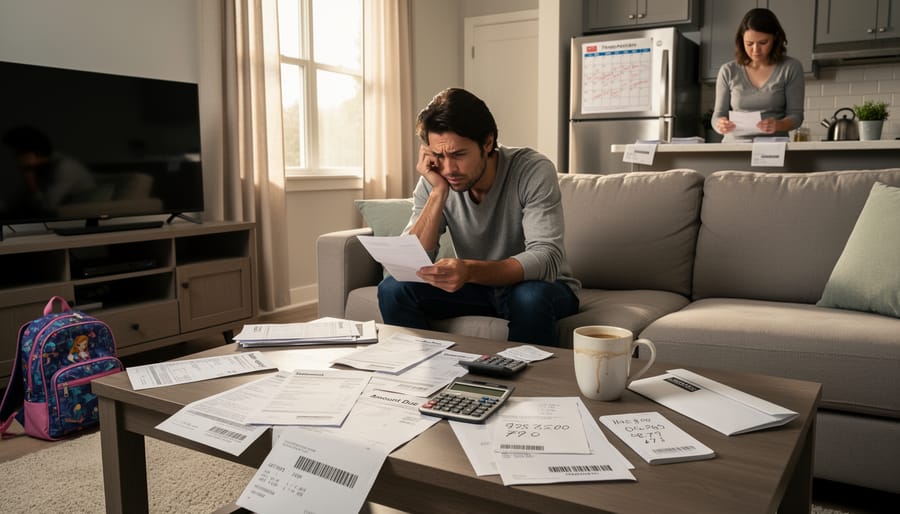

A $300 emergency isn’t theoretical for Canada’s financially marginalized, it’s the difference between keeping the lights on and sitting in the dark. Sociological research reveals that these seemingly modest amounts represent survival thresholds rather than discretionary spending crises.

For a single mother working part-time in Winnipeg, $300 covers an unexpected car repair that determines whether she can reach her workplace. Without the vehicle, she loses shifts; without income, she faces eviction. The payday loan becomes a rational choice within constrained circumstances, not evidence of poor financial planning.

Low-income international students face similar pressures. Already stretched by the cost of studying in Canada an unexpected dental emergency or laptop breakdown can derail their academic progress entirely. The $300 loan covers the immediate crisis but initiates a debt cycle: repayment takes priority over groceries, creating new shortfalls that require new loans.

Utility disconnection notices represent another common $300 emergency. A Toronto study found that households borrowing for utility payments were three times more likely to experience repeat borrowing within six months. The pattern reveals how survival debt operates: borrowers aren’t spending frivolously but managing cascading crises within systemically inadequate incomes. Each $300 loan addresses an immediate threat while simultaneously creating the conditions for future borrowing, illustrating how structural poverty manufactures individual debt traps.

The Debt Trap Mechanism

The debt trap mechanism operates through structural features embedded in payday loan design rather than borrower irresponsibility. When a $300 loan comes due, typically within two weeks, the borrower must repay the principal plus fees that can reach $45 to $60 depending on provincial regulations. For someone living paycheque to paycheque, allocating $345 to $360 from their next pay creates an immediate shortfall that necessitates another loan.

This cycle perpetuates itself through what sociologists term “churning,” where lenders profit from serial renewals rather than one-time transactions. Industry data reveals that a substantial portion of payday loan revenue derives from borrowers taking out ten or more loans annually, often with the same lender. The business model depends on repeat customers trapped in recurring debt obligations.

From a structural perspective, the trap reflects systemic wage stagnation and eroded social safety nets rather than poor money management. Borrowers face impossible mathematics: income insufficient to cover basic needs, unexpected expenses that traditional credit cannot address, and loan terms that extract resources faster than precarious employment can replenish them. The mechanism functions as a poverty tax, systematically transferring wealth from financially vulnerable populations to corporate lenders while maintaining the illusion of consumer choice. This structural entrapment reveals how payday lending operates as a form of financial extraction that both responds to and reinforces economic marginalization.

Racialization, Gender, and Payday Lending

Indigenous Communities and Financial Services

Indigenous peoples in Canada face compounded barriers to mainstream financial services rooted in centuries of colonial policy and systemic exclusion. The Indian Act historically restricted economic autonomy for First Nations people, creating lasting distrust of formal banking institutions. Many reserves lack physical bank branches, forcing residents to travel significant distances for basic banking services. This geographic isolation, combined with lower average incomes and employment instability on reserves, creates conditions where payday lenders become one of few accessible credit options.

Urban Indigenous populations similarly experience financial marginalization. A 2019 study found that Indigenous people in Canadian cities are three times more likely to use payday loans than non-Indigenous residents, even when controlling for income. This disparity reflects intersecting disadvantages: discrimination in employment limits job stability, while racism in housing markets creates precarious living situations that generate financial emergencies. Indigenous women face particularly acute vulnerability, experiencing both gendered economic disadvantage and racialized exclusion from traditional credit.

The growth of online payday lending has paradoxically worsened access issues for remote communities. While digital platforms theoretically overcome geographic barriers, they often charge higher interest rates than storefront locations and operate with less regulatory oversight. For Indigenous borrowers already navigating financial systems designed without their participation, these loans represent not financial inclusion but rather exploitation of exclusion. The $300 loan threshold frequently covers emergency expenses like funeral costs or travel for medical appointments unavailable on reserve, expenses that reveal gaps in social services rather than individual financial mismanagement.

Newcomers and Precarious Immigration Status

Recent immigrants and temporary residents in Canada face a distinctive constellation of barriers that funnel them toward payday lenders, even when they arrive with education, professional credentials, and financial stability in their home countries. The Canadian credit system effectively renders these individuals financially invisible: without a domestic credit history, newcomers cannot access mainstream loans, credit cards, or even basic banking services that established residents take for granted. A skilled engineer from India or a healthcare professional from the Philippines may find themselves unable to rent an apartment, finance a vehicle for work, or cover unexpected expenses through conventional channels.

Temporary foreign workers occupy an even more precarious position. Their work permits tie them to specific employers, creating a power imbalance that can result in wage theft, unsafe conditions, or sudden job termination without recourse. When employers withhold pay or unexpected costs arise, these workers cannot wait for traditional loan approvals that may require permanent residency documentation. A $300 payday loan becomes the only accessible option to cover rent, send remittances home, or address emergencies.

Immigration status itself creates vulnerability. Those with pending applications, expired permits, or precarious legal standing avoid interactions with institutions that might report them to immigration authorities. Payday lenders ask fewer questions and demand less documentation, offering anonymity that banks cannot provide. This financial exclusion is not incidental but structural, reflecting how Canadian systems prioritize certain bodies while marginalizing others based on citizenship status and perceived belonging.

Theoretical Frameworks for Understanding Payday Loans

Sociological analysis of payday loans requires moving beyond individual-choice narratives to examine the structural forces that create and sustain demand for high-cost credit. Several theoretical frameworks, commonly explored in sociology schools in Canada and through social sciences degrees provide essential lenses for understanding why payday loans concentrate among vulnerable populations.

- Financialization

- The increasing dominance of financial motives, markets, and institutions in everyday life, transforming basic survival needs into debt relationships. Payday loans represent the penetration of finance capital into the most precarious corners of economic existence.

- Predatory Inclusion

- The process by which marginalized groups gain access to financial services, but only on exploitative terms that extract wealth rather than build it. This framework explains how payday lenders appear to serve excluded populations while actually deepening their disadvantage.

- Poverty Premium

- The phenomenon whereby low-income individuals pay more for essential goods and services, including credit, due to their economic position. A $300 payday loan with 400% APR exemplifies how being poor becomes expensive.

- Social Exclusion

- The structural processes that prevent individuals and groups from full participation in social, economic, and political life. Financial exclusion from mainstream banking creates the conditions for payday loan dependence.

- Neoliberal Governance

- The political rationality that emphasizes individual responsibility, market solutions, and minimal state intervention in economic affairs. This framework positions financial problems as personal failures rather than systemic outcomes requiring collective response.

These concepts intersect to explain payday lending as a structural phenomenon rather than a collection of poor choices. Social exclusion theory illuminates how barriers to traditional banking, stable employment, and living wages create populations with urgent cash needs but no legitimate credit options. Financialization theory contextualizes payday loans within broader patterns of debt penetration into working-class life, where wages no longer cover basic reproduction costs and credit fills the gap. The neoliberal governance framework, meanwhile, reveals how regulatory approaches treat borrowers as rational consumers making informed choices, ignoring power imbalances and desperation.

Research methods taught at anthropology universities complement these theoretical perspectives, particularly ethnographic approaches that document lived experiences of financial precarity. Unlike understanding pop culture trends that may reflect voluntary consumption patterns, analyzing payday loan use requires recognizing constraints that limit meaningful choice. The theoretical sophistication lies in explaining how seemingly individual transactions reflect structured inequality, where $300 loans become necessary survival mechanisms within capitalism’s failures to provide adequate wages, social supports, or affordable housing.

Comparative Perspectives: France and International Context

France’s regulatory approach to short-term consumer credit stands in marked contrast to Canada’s payday loan landscape. French law caps the annual percentage rate on all consumer loans at rates that make the traditional North American payday loan model economically unviable for lenders. The country’s usury laws, updated quarterly by the Banque de France, typically limit interest rates to approximately one-third above the average market rate for each loan category. This creates a ceiling around 20% APR for small personal loans, compared to effective annual rates exceeding 500% common in Canadian payday lending.

Beyond rate caps, France maintains a robust social safety net that addresses the income volatility driving payday loan demand in Canada. The Caisse d’Allocations Familiales administers emergency grants and interest-free loans for households facing unexpected expenses. Municipal social service centres provide crisis funds without requiring repayment. These interventions function as preventive measures against debt cycles rather than responses to existing over-indebtedness.

The United Kingdom offers another instructive model through the Financial Conduct Authority’s 2015 reforms. The FCA implemented a total cost cap limiting fees and interest to 100% of the principal borrowed, alongside restrictions on rollover loans. Research following these changes showed dramatic reductions in repeat borrowing without evidence of increased loan shark activity, contradicting industry predictions. Lenders adapted by tightening credit assessments and encouraging longer-term installment products with lower effective rates.

Australia’s shift toward comprehensive credit reporting allows lenders to assess affordability using fuller financial pictures, reducing predatory lending while maintaining access. Japan virtually eliminated payday lending through combined interest rate caps and mandatory affordability assessments in 2006. These international examples demonstrate that alternative regulatory frameworks can address the financial needs payday loans purport to serve while minimizing exploitation of vulnerable populations. The persistence of high-cost lending in Canada reflects policy choices rather than inevitable market forces.

The evidence presented throughout this analysis demonstrates that $300 payday loans serve as a diagnostic tool for understanding structural inequalities in Canadian society. These small-denomination loans reveal systematic failures in employment security, social safety nets, and financial inclusion rather than individual financial mismanagement. When working Canadians cannot absorb a $300 emergency without turning to high-cost credit, this signals fundamental problems with income distribution, labour market precarity, and the erosion of economic buffers that once protected vulnerable populations.

A sociological lens reframes payday lending as a symptom of financialization and neoliberal governance, where individuals bear responsibility for risks that previous generations understood as collective concerns. The concentration of payday lenders in racialized neighbourhoods, the overrepresentation of Indigenous borrowers, and the gendered dimensions of financial vulnerability are not coincidental patterns but predictable outcomes of intersecting systems of oppression. These loans function as expensive band-aids on wounds created by inadequate wages, housing unaffordability, and discriminatory access to mainstream financial services.

Moving forward, policymakers must resist the temptation to address payday lending solely through interest rate caps or consumer education. While these measures have merit, they treat symptoms rather than causes. Meaningful reform requires confronting income inequality, expanding social housing, strengthening employment standards, and ensuring universal access to affordable credit. Financial regulation must be paired with robust welfare provisions and living wages.

For scholars engaged in study and research in Canada payday loans offer fertile ground for examining how market-based solutions to social problems create new forms of exploitation. Future research should deepen intersectional analyses, track longitudinal impacts of borrowing patterns, and evaluate alternative models of financial inclusion. Only by understanding payday loans as a social justice issue can Canada develop equitable solutions that address root causes rather than merely managing the consequences of systemic inequality.